'CER (Carbon Emission Reduction) trading' based business model-- which has manifested itself in Govt Of India's 'Bachat Lamp Yojna' -- has been enabled by few important happenings in the recent past

1. The Clean Development Mechanism (CDM) of the United Nations allows a country with an emission reduction commitment under the Kyoto Protocol to implement an emission reduction project in developing countries. In such projects, emission so reduced can be converted to saleable credits known as CERs (carbon Emission reduction). Each CER certificate is equivalent to a tonne (1000 Kgs) of carbon dioxide, which can be counted towards meeting Kyoto Protocol targets. Emerging markets like India and China are among the largest credit generators. The users are industrialized countries where companies, rather than reducing emissions, will buy such credits and meet their emission reduction target

2. Being amongst the ‘’big four’’ polluters of the World, Govt of India sets itself an ambitious target of cutting the carbon intensity by 24% by 2020. As per Govt of India’s 2009 report, which is based on independent studies by 5 organizations, India’s current carbon emission stands at 1.9 Bn tons and expected to grow to 30 Bn tons by 2030.

3. Infrastructure sector in India contributes 58 per cent to the country’s total greenhouse gas (GHG) emissions (Source: India Infrastructure report 2010). Therefore a large part of the government’s effort towards low-carbon growth is being directed in the power sector, since electricity contributes 38 per cent to the gross emissions of 1.9 Bn tonnes of carbon dioxide equivalent. Bureau of Energy Efficiency (BEE) gets established in March 2002, as a statutory body by the Government of India under the Energy Conservation Act 2001. The agency's function is to develop programs which will increase the conservation and efficient use of energy in India.

4. Carbon Emission Reduction (CER) is treated in the derivative trading market as a commodity. In India this is new commodity to be traded in Indian derivative market. Starts trading in National Commodity and Derivatives Exchange Ltd (NCDEX), India from the month of April, 2008

Joining the dots, BEE designed an innovative business model to give a push to carbon emission reduction and energy efficiency improvement initiatives in India.

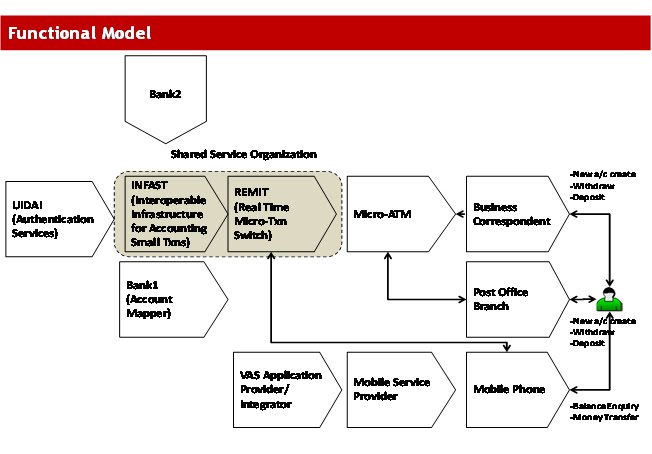

Value chain below depicts BEE’s working model to deliver on the mandate to reduce carbon emission in India

To replace incandescent bulbs with compact florescent lamps (CFL) all across the country is one such important initiative by the BEE. Usage of incandescent lamps has contributed a great deal to Green House Gases (GHG) emissions. The Bureau Energy Efficiency (BEE) has estimated that more than 400 million incandescent light bulbs (ICLs) are used in India, which is an extremely energy inefficient form of lighting, with just 5 percent of the electricity input converted to light. These lamps are harmful to the environment because they use so much energy to function. Most of the energy is emitted as heat and not as light and leaves larger carbon foot print. If the incandescent lamps are replaced with the efficient Compact Fluorescent Lamps (CFLs) which consume only 1/4th to 1/5th of the energy used by ICLs and provide the same level of light, it will save 6000 MW of energy and Rs 24000 crore per annum. The replacement of 400 million ICLs with CFLs will reduce 20 million tonnes of carbon dioxide from grid connected power plants.

To replace incandescent bulbs with compact florescent lamps (CFL) all across the country is one such important initiative by the BEE. Usage of incandescent lamps has contributed a great deal to Green House Gases (GHG) emissions. The Bureau Energy Efficiency (BEE) has estimated that more than 400 million incandescent light bulbs (ICLs) are used in India, which is an extremely energy inefficient form of lighting, with just 5 percent of the electricity input converted to light. These lamps are harmful to the environment because they use so much energy to function. Most of the energy is emitted as heat and not as light and leaves larger carbon foot print. If the incandescent lamps are replaced with the efficient Compact Fluorescent Lamps (CFLs) which consume only 1/4th to 1/5th of the energy used by ICLs and provide the same level of light, it will save 6000 MW of energy and Rs 24000 crore per annum. The replacement of 400 million ICLs with CFLs will reduce 20 million tonnes of carbon dioxide from grid connected power plants.

Soon enough, BEE realized that the key impediment in voluntary adoption of the CFL was prohibitively high market price of CFL (INR 100/bulb) vis-à-vis ICL (INR 15/bulb). How to bridge this gap of INR 85 in the market price of CFL and ICL was the key question facing BEE. What is known as ‘Bachat Lamp Yojna’ (BLY) is really an innovative business model that addresses the issue of market price differential between CFL and ICL lamps. This is made possible by way of selling the resultant carbon credits (CER) (where each unit of CER is equivalent to the reduction of 1000 Kgs of CO2 or its equivalent), generated by replacing CFLs with ICLs to the Clean Development Mechanism (CDM) set up under Kyoto protocol

Key risk to this CDM based business model is due to prevailing price volatility for CER prices on the European Energy Exchange (EEE), Europe being the biggest consumer of CERs generated in India. Historical data re price movement of the CER shows that individual CER prices have actually moved between 24 euros to 3 euros over last 4 years. Developing nations like India and China generate substantial amount of CERs have devised various mechanisms to guard against the price volatility including holding the CERs back in anticipation of price recovery in the European Commodity Markets.

1. The Clean Development Mechanism (CDM) of the United Nations allows a country with an emission reduction commitment under the Kyoto Protocol to implement an emission reduction project in developing countries. In such projects, emission so reduced can be converted to saleable credits known as CERs (carbon Emission reduction). Each CER certificate is equivalent to a tonne (1000 Kgs) of carbon dioxide, which can be counted towards meeting Kyoto Protocol targets. Emerging markets like India and China are among the largest credit generators. The users are industrialized countries where companies, rather than reducing emissions, will buy such credits and meet their emission reduction target

2. Being amongst the ‘’big four’’ polluters of the World, Govt of India sets itself an ambitious target of cutting the carbon intensity by 24% by 2020. As per Govt of India’s 2009 report, which is based on independent studies by 5 organizations, India’s current carbon emission stands at 1.9 Bn tons and expected to grow to 30 Bn tons by 2030.

3. Infrastructure sector in India contributes 58 per cent to the country’s total greenhouse gas (GHG) emissions (Source: India Infrastructure report 2010). Therefore a large part of the government’s effort towards low-carbon growth is being directed in the power sector, since electricity contributes 38 per cent to the gross emissions of 1.9 Bn tonnes of carbon dioxide equivalent. Bureau of Energy Efficiency (BEE) gets established in March 2002, as a statutory body by the Government of India under the Energy Conservation Act 2001. The agency's function is to develop programs which will increase the conservation and efficient use of energy in India.

4. Carbon Emission Reduction (CER) is treated in the derivative trading market as a commodity. In India this is new commodity to be traded in Indian derivative market. Starts trading in National Commodity and Derivatives Exchange Ltd (NCDEX), India from the month of April, 2008

Joining the dots, BEE designed an innovative business model to give a push to carbon emission reduction and energy efficiency improvement initiatives in India.

Value chain below depicts BEE’s working model to deliver on the mandate to reduce carbon emission in India

Soon enough, BEE realized that the key impediment in voluntary adoption of the CFL was prohibitively high market price of CFL (INR 100/bulb) vis-à-vis ICL (INR 15/bulb). How to bridge this gap of INR 85 in the market price of CFL and ICL was the key question facing BEE. What is known as ‘Bachat Lamp Yojna’ (BLY) is really an innovative business model that addresses the issue of market price differential between CFL and ICL lamps. This is made possible by way of selling the resultant carbon credits (CER) (where each unit of CER is equivalent to the reduction of 1000 Kgs of CO2 or its equivalent), generated by replacing CFLs with ICLs to the Clean Development Mechanism (CDM) set up under Kyoto protocol

Key risk to this CDM based business model is due to prevailing price volatility for CER prices on the European Energy Exchange (EEE), Europe being the biggest consumer of CERs generated in India. Historical data re price movement of the CER shows that individual CER prices have actually moved between 24 euros to 3 euros over last 4 years. Developing nations like India and China generate substantial amount of CERs have devised various mechanisms to guard against the price volatility including holding the CERs back in anticipation of price recovery in the European Commodity Markets.

{kind=link}