Let’s look at 3 disparate data pointsData point No 1: - India has close to 90 million farmer households (Ref: National Sample Survey. In 2001, average Indian household consisted of 5.4 people in rural areas and 5.2 people in urban areas). Of these, around 51% don’t have access to any credit from either institutional or non-institutional sources. Only 27% households are indebted to formal sources.

Data point No 2:- ‘No-frills’ accounts offered by banks in the recent past have not been very successful in terms of achieving financial inclusion of the unbanked populace. Given the typical cost-to-serve ratios in sparsely populated rural areas, banks find it extremely difficult to operate larger number of tiny accounts as well as micro-transactions profitably. A bank branch in India serves about 16000 people in India. This number is very high as compared to developed countries

Data point No 3:-Wireless telephony penetration rate in India is the highest in the world. As per TRAI (Telecom Regulatory Authority of India), number of mobile subscribers in India-as of Mar’11-is 811.59million (~81cr), growing at a healthy 3% month-on-month rate. The share of urban subscribers stands at 66% (~54cr) and the rest @34% (~27cr) comes from the rural area.

What do these data points indicate?

These data points, looked at in a joined up manner, indicate that 27cr rural Indians possess mobile phones but more than 50% (>14Cr) of these don’t have access to any credit from either institutional or non-institutional sources. In nutshell, there is a significant opportunity for banks to expand in rural areas, provided some innovation in business model is able to rationalize the cost-to-serve ratio for the aspiring banks

What are the key components of New Business Model for Banks?New business model for ensuring financial inclusion is shown in adjoining figure. Key value proposition is ‘no-frills’ account for rural unbanked people of India.

What are the key components of New Business Model for Banks?New business model for ensuring financial inclusion is shown in adjoining figure. Key value proposition is ‘no-frills’ account for rural unbanked people of India.

Besides Business Correspondent s and Sub-BCs, mobile phones and Micro-ATMs form an important distribution channel. Other than that the fact that Indian Post Office has over 1, 50,000 branches, of which more than 70% being located in rural India, presents an attractive option to banks for an alternate distribution channel. There is an opportunity for banks to leverage Post office’s rural presence for the effective service distribution at lower cost-to-serve ratio.

On the supply side, participating banks can form a ‘shared services organization’ (a la tower sharing companies in telecom sector) for creating and maintaining an interoperable infrastructure for small transaction accounting etc which will help take out the service delivery cost significantly. UIDAI being the key enabler in terms of providing authentication services for online mobile banking transactions. UIDAI services could be availed on transaction based costing model.

Data point No 2:- ‘No-frills’ accounts offered by banks in the recent past have not been very successful in terms of achieving financial inclusion of the unbanked populace. Given the typical cost-to-serve ratios in sparsely populated rural areas, banks find it extremely difficult to operate larger number of tiny accounts as well as micro-transactions profitably. A bank branch in India serves about 16000 people in India. This number is very high as compared to developed countries

Data point No 3:-Wireless telephony penetration rate in India is the highest in the world. As per TRAI (Telecom Regulatory Authority of India), number of mobile subscribers in India-as of Mar’11-is 811.59million (~81cr), growing at a healthy 3% month-on-month rate. The share of urban subscribers stands at 66% (~54cr) and the rest @34% (~27cr) comes from the rural area.

What do these data points indicate?

These data points, looked at in a joined up manner, indicate that 27cr rural Indians possess mobile phones but more than 50% (>14Cr) of these don’t have access to any credit from either institutional or non-institutional sources. In nutshell, there is a significant opportunity for banks to expand in rural areas, provided some innovation in business model is able to rationalize the cost-to-serve ratio for the aspiring banks

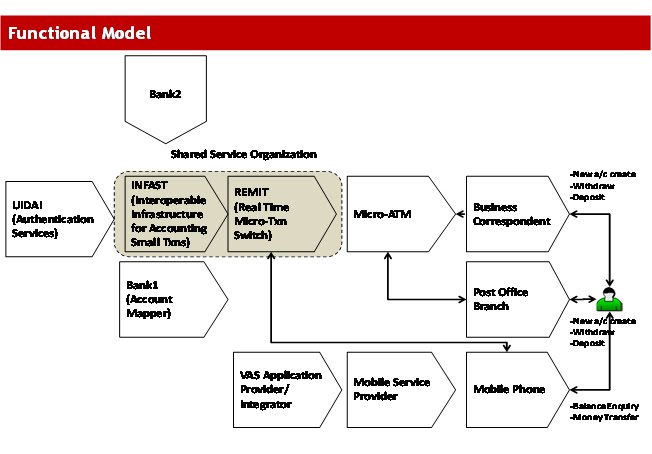

What are the key components of New Business Model for Banks?New business model for ensuring financial inclusion is shown in adjoining figure. Key value proposition is ‘no-frills’ account for rural unbanked people of India.

What are the key components of New Business Model for Banks?New business model for ensuring financial inclusion is shown in adjoining figure. Key value proposition is ‘no-frills’ account for rural unbanked people of India.Besides Business Correspondent s and Sub-BCs, mobile phones and Micro-ATMs form an important distribution channel. Other than that the fact that Indian Post Office has over 1, 50,000 branches, of which more than 70% being located in rural India, presents an attractive option to banks for an alternate distribution channel. There is an opportunity for banks to leverage Post office’s rural presence for the effective service distribution at lower cost-to-serve ratio.

On the supply side, participating banks can form a ‘shared services organization’ (a la tower sharing companies in telecom sector) for creating and maintaining an interoperable infrastructure for small transaction accounting etc which will help take out the service delivery cost significantly. UIDAI being the key enabler in terms of providing authentication services for online mobile banking transactions. UIDAI services could be availed on transaction based costing model.

{kind=link}